Scope 3 emissions under AASB S2: from voluntary to mandatory

What Australia’s mandatory climate reporting standard means for your value chain emissions.

To date, scope 3 emissions reporting has been voluntary and ‘nice to have’. The Australian mandatory climate reporting standard (AASB S2) have shifted the dial Scope 3 emissions are now mandatory. With the scope of the requirements increasing over time, it’s time to get into the detail of Scope 3.

About AASB S2

The Australian Sustainability Reporting Standards (ASRS) were issued by the Australian Accounting Standards Board (AASB) in September 2024. They are based on the International Sustainability Standards Board (ISSB), adapted for Australian law. There are two standards:

AASB S1 (General Requirements) is a voluntary standard covering sustainability aspects (other than climate) broadly. These may other environmental impacts such as air quality, water, ecological impacts or other social or governance indicators.

AASB S2 (Climate-related Disclosures) is a mandatory standard setting out exactly what entities must disclose about climate-related risks and opportunities.

Since AASB S2 is mandatory, it is the standard that needs immediate attention. You can read it in full on the AASB website.

Key requirements of AASB S2: The four pillars

Overview of AASB S1 and AASB S2 | April 2025

https://aasb.gov.au/research-resources/knowledge-hub/aasb-s2-knowledge-hub/aasb-s2-guidance/

The AASB S2 follows the four-pillar framework provided by the Taskforce on climate-related Financial Disclosures (TCFD) which includes Governance, Strategy, Risk Management, and Metrics and Targets. As the standard focuses on climate, greenhouse gas (GHG) emissions as the key environmental indicator of climate change sits at its centre. In practice, entities must measure their emissions, set out how emissions inform strategy and targets, and show how all of this is governed.

Governance: The board and management processes used to oversee climate-related risks and opportunities, including who is responsible and how often climate is considered.

Strategy: The material climate risks and opportunities, their current and anticipated financial effects, any transition plan, and the results of scenario analysis. AASB S2 requires testing against at least two scenarios, including one consistent with limiting warming to 1.5°C and one that exceeds 2°C.

Risk management: How climate risks are identified, assessed, prioritised, and monitored, and how this connects to the organisation's wider risk management.

Metrics and targets: Scope 1 and Scope 2 emissions from the first year, material Scope 3 emissions from the second year, and progress against any climate targets. Financial institutions must also disclose financed emissions. In short, entities must disclose the climate information that could reasonably affect their cash flows, access to finance, or cost of capital over the short, medium, or long term.

What are Scope 3 emissions

Scope 3 covers indirect emissions generated in upstream and downstream processes of the value chain, including manufacture and supply of goods purchased by, and the fates of products sold by, the reporting entity. For most organisations, estimating Scope 3 emissions is the hardest part due to the difficulty in collecting activity data and sourcing appropriate emission factors.

The Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Standard is the globally accepted Standard on Scope 3 emissions reporting and is relied upon by reporting standards, e.g., the ISSB Standards, AASB S2, Science Based Target Initiative (SBTi), the EU’s CRSD. It defines 15 categories of emissions across the value chain.

Scope 3 typically accounts for around 70-90% of a company’s total footprint, dominated by purchased goods and services and other supply chain activities. Reporting that ignores or underpays these emissions misses most of the picture; credible emissions reporting requires a meaningful understanding of the value chain.

Scope 3 emissions under AASB S2

| Group | First reporting period from | Revenue (or more) | Gross assets (or more) | Employees (or more) | Also captured |

|---|---|---|---|---|---|

| Group 1 | 1 January 2025 | $500 million | $1 billion | 500 | NGER reporters above the publication threshold in section 13 of the NGER Act 2007 |

| Group 2 | 1 July 2026 | $200 million | $500 million | 250 | Other NGER reporters; asset owners with $5 billion or more under management |

| Group 3 | 1 July 2027 | $50 million | $25 million | 100 | Smaller entities preparing a Chapter 2M financial report |

Quantifying Scope 3 emissions is required from the second year of reporting for companies in scope of the standard: FY27 for Group 1, FY28 for Group 2 and FY29 for Group 3. The size thresholds for each group are set out in the table.

As Group 1 entities enter their second year of reporting, they should already be building full value chain inventories. Entities in Groups 2 and 3 should be on the front foot and start mapping upstream and downstream emissions now.

Most small and medium businesses fall below the Group 3 thresholds and are not captured. The May 2026 Federal Budget proposed lifting the large proprietary company thresholds, which could move some smaller private companies out of scope. These changes remain subject to consultation and legislation.

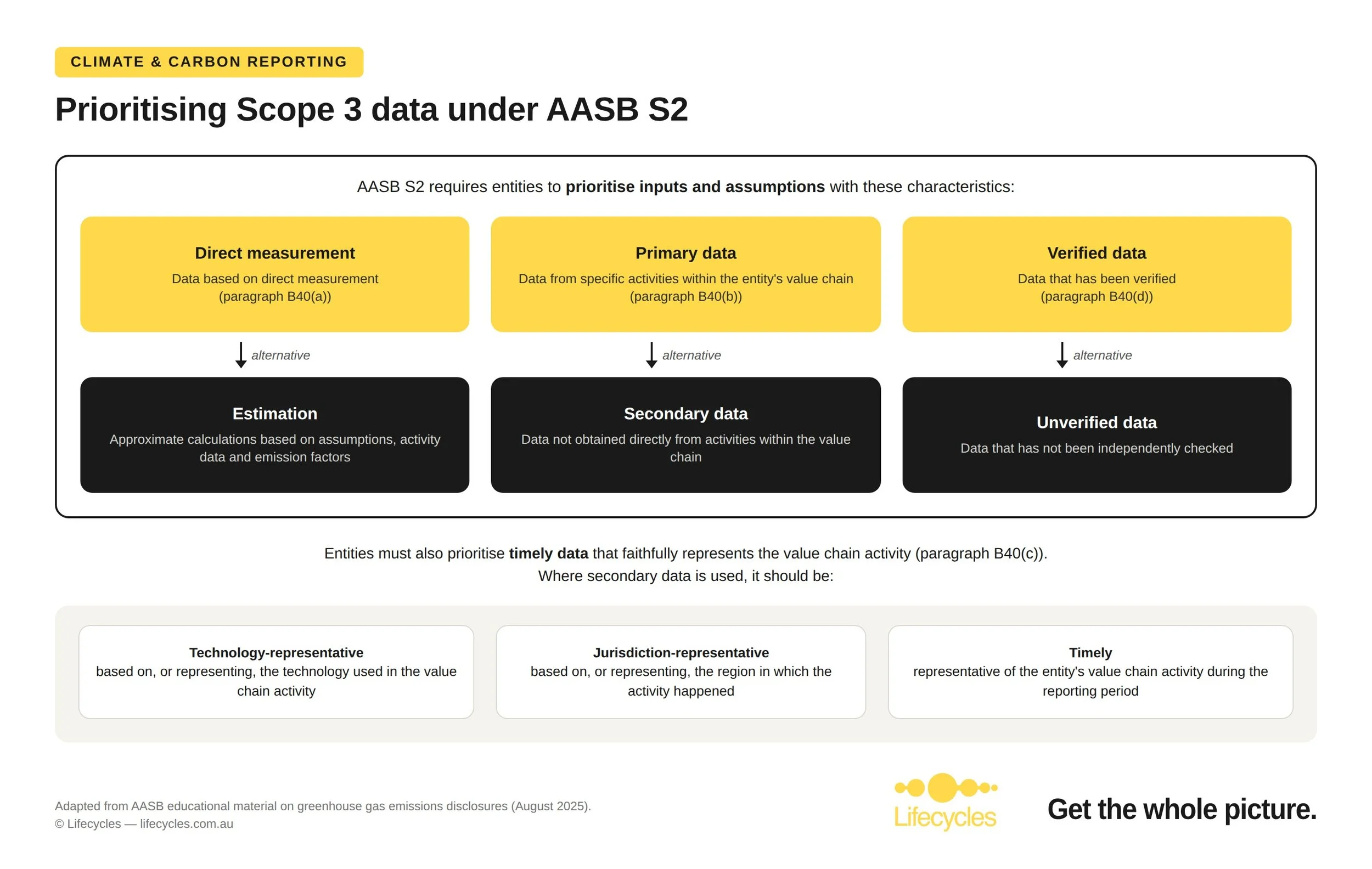

Prioritising Scope 3 data in AASB S2

AASB S2 requires an entity to consider all 15 categories of Scope 3 emissions set out in the GHG Protocol Corporate Value Chain (Scope 3) Standard.[1] It also requires entities to prioritise data in accordance with the following measurement framework:

At this stage, AASB S2 only requires targets for Scope 1 and Scope 2 emissions, though this could extend to Scope 3 into the future. Entities wanting a target validated by the Science-Based Targets Initiative (SBTi) will not have the choice: where value chain emissions exceed 40% of total emissions, SBTi requires Scope 3 to be included in the target.

What this means in practice

There are broadly three ways to quantify Scope 3 emissions, in descending order of accuracy and effort.

Supplier-specific: Emission factors derived from supplier-specific data (e.g. materials and energy inputs). The most accurate approach, but dependent on supplier engagement an data-sharing relationships that take time to build.

Life cycle inventory: published bottom-up LCA data, used directly or adjusted to fit the product category or material mix. Sources include ecoinvent, Australia Life Cycle Inventory (AusLCI) Australian Government National Greenhouse Accounts, IPCC. A strong balance of rigour and practicality for most categories.

Spend-based: top-down factors from environmentally extended input-output (EEIO) models such as EXIOBASE, applied to dollars spent. Fast and complete, but the least precise, and best treated as a screening tool.

Scope 3 reporting will be journey. In the early years, limited availability means a degree of reliance on spend-based estimates is normal. There are, however, important limitations to that reliance, and higher-quality data should be prioritised over time. Spend-based data allocates a generic emission factor to a dollar value. Emissions will be inflated wherever prices rise, meaning reported emissions can go up year-on-year even when real-world emissions are falling and genuine reductions (like switching to lower-carbon supplier) are invisible.

The absence of actual emissions data means that there is limited availability to set targets. For example: SBTi alignment is a genuine competitive advantage: in the SBTi’s own research, nine in ten companies with validated targets report positive business impacts, 95% cite an enhanced reputation with stakeholders and 80% say targets strengthened investor relations. Businesses without that credibility risk being outcompeted by those who have it.

Like many standards and certifications, it is no easy feat. Efforts to reduce Scope 3 emissions will not be recognised unless there are clear data and justifications to back them up.

As you build out your inventory, prioritise quality, as it provides the accurate picture and enables action on genuine emissions reduction.

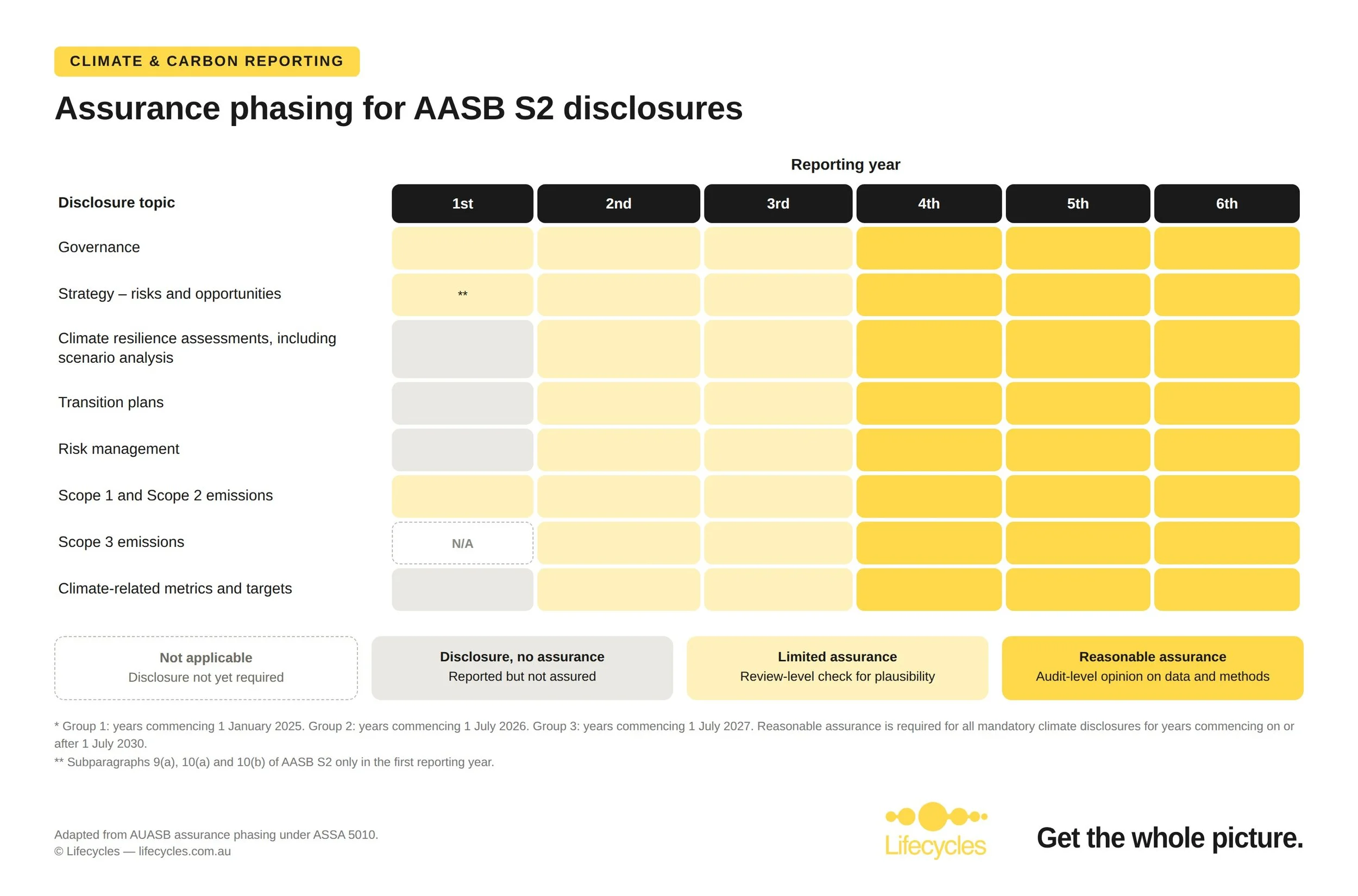

Assurance requirements

Scope 3 emissions must be assured for all groups, and the level of assurance increases over time. Limited assurance applies for the first three reporting years; from the fourth reporting year, reasonable assurance applies. The degree of scrutiny applied to an entity's Scope 3 data will intensify significantly, moving from a review-level check for plausibility under limited assurance to a full audit-level opinion under reasonable assurance, where auditors rigorously test the underlying data, methodologies, boundaries and assumptions before forming their view.

How to prepare

Whichever group you fall into, the practical steps are consistent:

Start now, not later: the earlier the groundwork, the smoother the path to reasonable assurance.

Define your boundary: understand which Scope 3 categories are material to your business before diving into data collection.

Close the gaps in your value chain inventory and shift away from spend-based estimates toward supplier-specific and life cycle data for material categories.

Engage suppliers early: data-sharing relationships take time to build and underpin higher-quality reporting.

Document as you go: methodology, boundaries and assumptions are exactly what auditors will scrutinise as assurance intensifies.

Treat data quality as a journey, not a one-off exercise.

Own it at the top: climate risk oversight needs to sit with the board and management, not just the sustainability team.

Think beyond compliance: better data means genuine emissions reduction, not just a tick in the box.

How Lifecycles can help

Lifecycles has over 30 years experiences working in supply chain emissions analysis. We can help you at any stage of your Scope 3 journey, whether you’re just starting to build an inventory or strengthening the quality of your reporting, we draw on deep expertise and extensive databases to provide you with high-quality data that demonstrates commitment and accountability in your emissions reporting. This article focuses on GHG emissions as the mandatory reporting requirement, but environmental impacts extend well beyond carbon, to water, ecosystems and resources. That is where life cycle assessment comes in. Reporting under AASB S1 is voluntary, but it signals a commitment to broader environmental action, and the same data foundations serve both. Learn more about our climate and carbon reporting services, or get in touch to talk through where your organisation stands.

Key message? From oversight to impact: know your risk, shape your strategy, prove your progress.

This article is general information, current as at July 2026, and is not legal, accounting, or financial advice. AASB S2 and the surrounding regulatory settings continue to evolve. Confirm your obligations against the current standards and seek professional advice for your circumstances.

References

AASB, AASB S2 Climate-related Disclosures (compiled, December 2025)

AASB, Educational material: Disclosure of greenhouse gas emissions (August 2025)

AUASB, Climate and sustainability assurance requirements approved (ASSA 5010)

GHG Protocol, Corporate Value Chain (Scope 3) Accounting and Reporting Standard

SBTi, The Impact of Setting Science-Based Targets on Businesses (2025)